Sections of this topic

Sections of this topic

Bluevine operates as a financial technology company that collaborates with institutions, including Coastal Community Bank, to provide FDIC-insured services tailored to the needs of small and medium-sized businesses.

Bluevine launched its operations in 2013 to provide a single online platform that unites business checking with lines of credit and a business credit card for fast and flexible banking solutions to entrepreneurs. The platform provides fee-free business checking combined with industry-leading APYs, rapid digital approvals, streamlined tools for invoicing, AP automation, and spending tracking.

The platform supports over 500,000 businesses while providing loans exceeding $14 billion by mid-2025. The platform offers fee-free business checking and industry-leading APYs, together with rapid digital approvals and streamlined tools for invoicing, AP automation, and spending tracking.

In this comprehensive Bluevine review, we break down exactly what you get (and what you don’t), how it compares to traditional and FinTech competitors, and whether it’s a smart choice for your business in 2025.

>> Fast, Flexible, Digital – Bluevine Is Built for You >>

Key Features of Bluevine Business Banking

Let’s dig into what sets Bluevine apart from other online business banks.

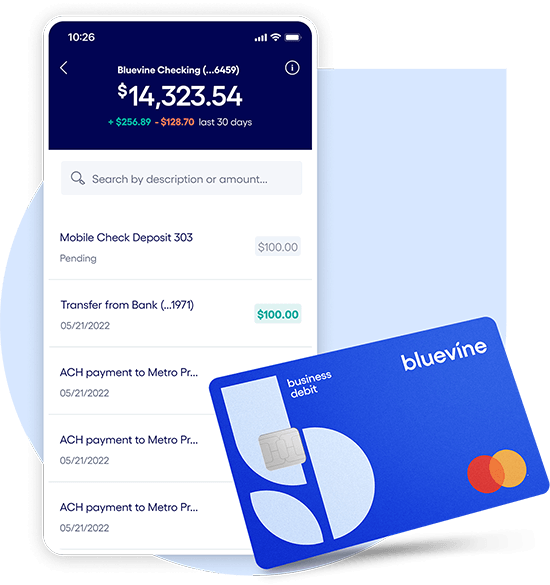

High-Yield Business Checking Account

Bluevine provides the most attractive interest-earning checking account solution available to business banking customers.

- The interest rate stands at 2.0% APY for balances up to $250,000 (as of 2025)

- The interest rate doesn’t apply to amounts exceeding $250,000.

- No interest earned beyond the $250K cap

- No monthly maintenance fees

- No minimum opening deposit

- The account earns interest without requiring any specific balance amount to stay active.

- Unlimited transactions (no per-transaction fees)

- Free ACH transfers

- Free incoming wires

- Free two checkbooks

- Free business debit card tied to your account

- The account provides access to 37,000+ MoneyPass® ATMs located throughout the United States

- The platform supports integration with QuickBooks, Xero, and additional accounting software solutions

The account structure of Bluevine creates an attractive option for entrepreneurs and freelancers who want to build their funds through passive growth without fees reducing their earnings.

Business Line of Credit

Bluevine offers a line of credit that stands out as a primary option for businesses requiring short-term financing flexibility.

- Borrow between $6,000 and $250,000

- The repayment period for this credit line extends to either 6 months or 12 months

- The interest rates begin at 6.2% (simple interest) and continue from there

- No prepayment penalty

- The funding process takes only 24 hours after approval to deliver the funds

- Apply completely online

- The revolving credit model allows your funds to automatically replenish after each repayment

- The financing option is available to businesses that generate at least $10,000 per month in revenue and have been operating for six months or more

The financing option works well for businesses that need to manage seasonal fluctuations, restock inventory, or respond to unexpected costs.

Online Bill Pay Tools

Manage vendor payments efficiently using Bluevine’s built-in bill payment platform.

- You can pay vendors through ACH transfers or wire transfers, or by sending them checks through the mail.

- The system allows you to monitor all your invoices and their corresponding due dates from a single dashboard.

- You can establish automatic payment schedules or make a single payment at a time.

- You can use your Bluevine balance to make payments or link an external account for transactions.

- The system allows you to send paper checks even though you never need to handle them personally.

- The ACH bill payment method is free, but you might need to pay small fees for wire transfers and checks.

The tool provides excellent benefits for simplifying your accounts payable operations when you need to handle multiple contractors or suppliers.

Mobile and Online Banking Experience

Bluevine has a well-designed digital experience, perfect for today’s mobile-first entrepreneurs.

Mobile app for Android and iOS

- Mobile check deposit feature

- Real-time balance and transaction notifications

- Push alerts for low balances, deposits, withdrawals, and payments

- Multi-user access with customizable roles and permissions

- Secure logins using biometrics (fingerprint, facial recognition)

- Full access to features via the web portal or mobile app

Their interface is clean and intuitive, making it easy to do your banking anywhere, anytime. suppliers.

Security & FDIC Insurance

Bluevine takes customer security and financial protection seriously.

- The accounts benefit from FDIC insurance protection, which extends to $3,000,000 through a network of partner banks beyond the standard $250,000 coverage

- Two-factor authentication (2FA) is available

- Data encryption and secure login protocols

- Regular third-party security audits

Cash Deposits via Green Dot®

While Bluevine is digital-first, it allows for cash deposits.

- Make deposits at 90,000+ Green Dot retail locations (like Walmart, Walgreens, CVS)

- Fee: Up to $4.95 per deposit, depending on the retailer

- The availability of cash depends on the specific location and the method used to load funds

The workaround for cash-based businesses isn’t ideal because it comes with fees and no in-network ATMs for deposits.

>> Experience Smarter Business Banking With Bluevine >>

Bluevine Pros and Cons

Bluevine Pros

- Earn Industry-Leading Interest on Checking: Traditional business banks provide their customers with interest rates that amount to 0% or nearly zero percent. The 2.0% APY offered by Bluevine for balances up to $250,000 makes this account an attractive option for businesses to store their funds.

- Truly No-Fee Structure: Startups and cost-conscious businesses will find this account perfect because it has no monthly fees, no minimum balance requirements, and no hidden charges.

- Access to Flexible Working Capital: The line of credit provided by this company stands as one of the most accessible funding options for small businesses since it offers quick applications and immediate funding, along with reasonable interest rates to businesses with imperfect credit profiles.

- Great Digital Experience: The platform of Bluevine offers a modern interface that users can access through both mobile and desktop devices. The entire process from account creation to daily operations runs smoothly without any interruptions.

- Vendor and Invoice Management: The built-in bill pay features enable fast payment of invoices and automated recurring payments while tracking due dates without requiring additional software.

- Generous FDIC Insurance: The FDIC protection through Bluevine’s partner sweep network extends up to $3 million, which provides businesses with extra security for their large cash reserves.

- Quick and Easy Account Setup: Most users can establish an account within a period of less than ten minutes. You will need your EIN, together with business documents and a valid ID, to complete the application.

- Multi-User Access: The system at Bluevine enables business owners to grant defined access permissions to team members, while most fintech competitors don’t offer this feature, which suits growing teams.

Bluevine Cons

- No Physical Branches: The 100% digital banking system of Bluevine will be unappealing to customers who want to conduct banking activities in person or require frequent teller assistance.

- Cash Deposit Limitations: The process of cash deposit requires using Green Dot as a third-party service, which imposes fees and provides less convenient and immediate banking services than traditional branch banking.

- No Zelle or Instant Transfers: The inability to use Zelle for money transfers represents a major drawback for users who depend on peer-to-peer payment tools. ACH is fast but not instant.

- No Joint Accounts: The current business account system at Bluevine restricts each account to having only one primary account owner.

- No Savings Account or Credit Card: The business savings account and branded credit card services aren’t available at Bluevine in 2025, which restricts complete financial planning capabilities.

- Customer Service Can Be Hit or Miss: The customer support team operates from Monday to Friday between 8 am–8 pm ET, but doesn’t provide 24/7 assistance. Users experience delayed responses and challenges when trying to reach live support.

>> Fast, Flexible, Digital – Bluevine Is Built for You >>

A Closer Look at Bluevine’s Line of Credit

The Bluevine business line of credit stands out as a major advantage over standard banking services because of its adaptable features. The service provides small business owners with instant working capital access through a revolutionary process that eliminates complex requirements.

What Makes It Different?

Traditional banks require their customers to undergo a prolonged credit application process, which includes paperwork and credit checks, interviews, and extended waiting periods for approval. Bluevine provides a digital-first credit application process that delivers fast and transparent service to businesses of all ages.

The approved borrowers can obtain between $6,000 and $250,000 with loan terms extending from 6 to 12 months. The line functions as revolving credit, so once you repay what you borrow, the credit becomes available again, no need to reapply.

Smart Use Cases for Bluevine’s Credit Line

Here are real-world scenarios where Bluevine’s credit line is especially helpful:

- Covering payroll during seasonal slumps

- Buying bulk inventory to qualify for supplier discounts

- Bridging invoice gaps in B2B operations

- Financing equipment repairs or upgrades

- Launching marketing campaigns when cash is tight

>> Open Your Bluevine Account Today! >>

How Bluevine Compares to Traditional Banks

Fees

- Traditional banks impose monthly maintenance fees ranging from $10 to $25 and charge penalties for overdrafts and set transaction limits at 200 free monthly transactions, followed by $0.25 per transaction.

- Bluevine offers its users no monthly fees, no minimum balance requirements, and unlimited transaction capabilities.

Verdict: Bluevine is the winner for fee-conscious entrepreneurs.

Interest Earnings

- Traditional banks provide business checking accounts with interest rates ranging between 0.01% and 0.05% APY.

- Bluevine provides 2.0% APY on balances up to $250,000.

Verdict: Bluevine dominates for earning passive income from your business funds.

Access and Convenience

- Traditional banks provide their customers with face-to-face service, which remains important for business owners who need to deposit cash, seek advice, and build banking relationships.

- The entire Bluevine platform operates online, which requires you to handle all transactions through digital means.

Verdict: Traditional banks win here, especially if your business handles frequent cash or prefers face-to-face service.

Account Opening and Convenience

- Traditional banks need customers to visit their branches in person before account opening, while also requiring documentation and extended waiting periods.

- You can create a Bluevine account through their website without needing to visit a branch, and the process takes only minutes.

Verdict: Bluevine is far more convenient for busy entrepreneurs.

>> Fast, Flexible, Digital – Bluevine Is Built for You >>

Bluevine Integrations and Business Tools

Bluevine is more than just a business checking account. It’s also a lightweight financial hub that connects with the tools you already use. While it may not offer the overwhelming suite of products found in traditional banks, it integrates smoothly with essential platforms, making everyday business operations easier, faster, and more organized.

Here’s a closer look at how Bluevine’s digital tools and integrations work for entrepreneurs, freelancers, and growing teams.

Accounting Software Integration

The most valuable feature of Bluevine’s ecosystem is its seamless connection to cloud-based accounting platforms. The automatic transaction syncing feature between QuickBooks Online and other accounting software enables businesses to view their deposits, withdrawals, and expenses in real-time. This helps prevent manual errors and simplifies month-end reconciliation. The system also allows expense categorization, which enables users or their bookkeepers to create current reports instantly.

Xero users also benefit from similar functionality through synchronized bank feeds, which enable them to easily match transactions and maintain clean books. FreshBooks users can connect to their banking activity through Plaid or Zapier services to achieve similar alignment between their banking and invoicing systems, even though it isn’t natively supported. Service-based professionals who invoice clients find this feature particularly useful because it enables them to maintain full control over incoming payments.

The accounting integrations provided by Bluevine eliminate the requirement for manual entry and reconciliation, thus saving businesses hours of work each month and making tax preparation less complicated. The direct link between your accounting software and your financial management system improves accuracy while reducing back-office labor costs, regardless of whether you handle your finances personally or work with a CPA.

Payment Processor Compatibility

The integration of Bluevine with major payment platforms is essential for businesses that conduct online sales or digital invoicing operations. Business owners can link their Bluevine business checking account to Stripe, PayPal, Square, and Shopify Payments to receive direct interest-earning payouts. The combined system allows businesses to manage their funds in one place while generating interest on their money until they need it.

Freelancers and contractors who use Upwork or Fiverr can direct their payments to Bluevine as their payout destination to maintain separate business and personal financial accounts. The separation of business and personal finances through this setup becomes essential for budgeting, bookkeeping, and compliance purposes, especially for sole proprietors and new LLCs.

Bluevine differentiates itself through its ability to serve as a versatile financial endpoint. Bluevine functions as a modern financial connector that links your revenue streams to your financial management tools instead of using traditional banks with limited digital economy integration.

Workflow Automation and Zapier Integration

The Bluevine platform doesn’t have a large app marketplace, but it does integrate with Zapier, which provides automation capabilities for more than 5,000 applications. Business owners can use Zapier to develop personalized workflows that decrease manual work and enhance monitoring capabilities.

The system allows you to send automated Slack notifications whenever your account receives transactions exceeding a specified amount. The system enables you to track all income in a shared Google Sheet so your business partner or virtual CFO can monitor cash flow in real-time.

The automation features of Bluevine prove especially useful for founders who handle various responsibilities. The connection between Bluevine and project management tools such as Trello or Notion through Zapier enables financial triggers that match project milestones. The automation system enhances productivity while transforming your banking operations into a valuable data source for making business decisions.

Zapier provides users with adaptable automation capabilities. The platform enables users to create a basic financial system that operates automatically, which saves time and minimizes errors while enhancing overall responsiveness.

Bluevine’s Support Team

Need assistance with your Bluevine business account? Their dedicated support team is ready to help with everything from account setup to troubleshooting.

- Phone Support: Call 888-216-9619 (Available Monday – Friday, 8:00 AM – 8:00 PM ET)

- Email Support: Reach out to [email protected] (You’ll typically receive a response within 1 business day.)

- Help Center: Explore helpful articles and FAQs at the Bluevine Help Center

- In-App & Web Support: Secure messaging is available directly through your Bluevine dashboard.

Whether you’re managing payments, reviewing transactions, or applying for financing, Bluevine’s support team is just a message or call away.

>> Open Your Bluevine Account Today! >>

Plans

Based on the image provided, Bluevine offers three business checking plans:

- Standard Plan: $0/month. Includes 1.5% APY on balances up to $250K, up to 5 sub-accounts, FDIC insurance up to $3M, free standard ACH, and unlimited transactions.

- Plus Plan: $30 or $0/month (waivable fee). Includes everything in the Standard plan, plus 2.7% APY on balances up to $250K, up to 10 sub-accounts, 20% off most Standard payment fees, 5 free printed and mailed checks/month, and 6 months free Xero subscription.

- Premier Plan: $95 or $0/month (waivable fee). Includes everything in the Plus plan, plus 3.7% APY on balances up to $3M, up to 20 sub-accounts, 50% off most Standard payment fees, 20 free printed and mailed checks/month, priority customer support, and access to treasury services.

>> Check Out the Best Pricing for Bluevine >>

Bluevine vs. Other FinTech Banks

Now let’s see how Bluevine stacks up against other popular online business banks: Novo, Lili, and Mercury.

Bluevine vs. Novo

- Bluevine provides 2.0% APY, but Novo doesn’t offer any interest payments

- The bill pay features are available on Bluevine, but Novo doesn’t provide this service

- Novo provides more third-party integrations with tools such as Stripe and Shopify

Bluevine vs. Lili

- Bluevine provides financial support to businesses operating under traditional structures and offers credit line options

- Lili provides tax tools specifically designed for freelancers and solo entrepreneurs

- The 2.0% APY makes Bluevine’s checking experience more robust than the others

Bluevine vs. Mercury

- Mercury provides its services to venture-backed startups and tech companies

- The platform Bluevine serves small businesses and contractors operating within the United States

- Mercury provides international wire transfer capabilities and treasury features but doesn’t support cash deposits

- The platform allows business credit and supports cash deposits through Green Dot

Who Should Use Bluevine?

Bluevine isn’t a one-size-fits-all bank, but for the right type of business owner, it offers incredible value, flexibility, and simplicity. Here’s who benefits most from banking with Bluevine:

Freelancers and Independent Contractors

- You need a separate business checking account to stay organized

- You want to earn interest on your balance instead of letting it sit idle

- You don’t want to deal with bank fees or paperwork

Bluevine provides control to writers, designers, consultants, and gig workers without adding unnecessary bulk to their operations.

Small Business Owners and LLCs

- Your business operates as a small company or e-commerce store with limited financial resources

- Your business requires a quick and dependable online banking system

- Your business requires occasional access to short-term funding and working capital

Bluevine provides excellent services to service providers and agencies, solopreneurs, and remote teams who want to avoid bank branches and maintain their business focus.

Startups and Digital-First Companies

- You are tech-savvy and do everything online

- You want an account that scales with your digital tools and software stack

- You need a credit line as a financial cushion, without having to pitch to a bank manager

If you’re in the early stages of building something, Bluevine helps you stay lean while maximizing your capital.

>> Open Your Bluevine Account Today! >>

Who Should Not Use Bluevine?

The Green Dot deposit method of Bluevine may be too restrictive or costly for businesses that handle large amounts of cash, such as restaurants and retailers. Businesses that require in-person services, including notary services, medallion signature guarantee, and complex loan structuring, won’t have access to physical branches. The current offerings of Bluevine don’t meet the needs of larger companies that require treasury management and escrow services, and corporate credit cards.

Real User Reviews: What Customers Are Saying?

Bluevine has built a solid reputation in the small business community, but like any service, it receives both praise and criticism. Here’s a look at what actual users are saying in 2025:

Positive Feedback

“Finally, a Business Account That Pays Me Back”

“I switched from Wells Fargo and couldn’t be happier. Earning 2% on my balance while avoiding monthly fees has made managing my cash flow so much easier.”

— Jason R., Marketing Consultant

“Smooth and Simple Setup”

“Opening my account took less than 10 minutes. The app is user-friendly, and I love that I can pay my contractors directly without any extra software.”

— Angela L., Freelance Web Developer

“The Line of Credit Saved Me”

“We hit a cash crunch in Q4, and Bluevine’s credit line was approved within 48 hours. It literally helped us stay afloat and fulfill our orders.”

— Marcus D., eCommerce Store Owner

Common Complaints

“Customer Service Needs Work”

“The banking platform is great, but I had a billing error, and getting in touch with support took over 48 hours. I wish they had weekend service.”

“Cash Deposits Are a Hassle”

“I run a mobile detailing business and still get paid in cash often. Using Green Dot to deposit funds is expensive and inconvenient compared to just walking into a bank.”

>> Check Out the Best Options for Bluevine >>

Is Bluevine Safe and Legit?

One of the most common questions readers ask is: “Can I really trust Bluevine with my business money?”

The answer is yes, and here’s why:

Backed by FDIC Insurance

Bluevine’s banking services are provided through Coastal Community Bank, Member FDIC. That means your deposits are:

- FDIC insured up to $250,000 per depositor, per ownership category

- Expanded to $3 million through Bluevine’s Sweep Network of partner banks

This setup uses the same multi-bank sweep system trusted by large institutions to protect high-dollar business deposits.

Bank-Level Security

Bluevine uses modern security standards and encryption protocols to keep your account safe.

- Two-Factor Authentication (2FA)

- TLS encryption for all web traffic

- Biometric login support (fingerprint, facial recognition) on mobile

- Regular third-party audits and vulnerability testing

Transparent and Regulated

- Bluevine is a registered financial technology provider operating under strict compliance frameworks.

- It’s not a fly-by-night startup—the company has been operating since 2013 and has raised over $700 million from reputable investors.

It partners with Coastal Community Bank and other regulated institutions for banking infrastructure and compliance.

Trust Ratings

- Better Business Bureau (BBB): A- A-rating

- Trustpilot: 4.2 stars (as of 2025)

Highly rated for security, digital experience, and ease of use

>> Join Business Communities Who Trust Bluevine >>

How to Open a Bluevine Account

Gone are the days of needing an in-person appointment and a stack of paperwork. With Bluevine, the entire process of opening a business checking account is fully online, and it usually takes less than ten minutes.

To begin, head over to Bluevine’s official website and click the “Open an Account” button. You’ll be guided to a short application form where you’ll enter your basic business and personal information, such as your full name, business name, business structure (like sole proprietorship or LLC), your Employer Identification Number (EIN) or Social Security Number (if you’re a sole prop), and contact details like your email, phone number, and business address.

Depending on your business type and industry, Bluevine might ask for supporting documents. These could include your Articles of Organization, a business license, or an operating agreement. Uploading these documents is easy; you can do it directly through the application portal or return later to complete it.

Identity verification is also part of the process. You’ll need to upload a valid government-issued photo ID (like a driver’s license or passport), and occasionally, Bluevine may request a quick selfie to confirm your identity. It’s all about keeping your account secure and compliant with banking regulations.

Once you’ve completed the application, Bluevine typically provides a decision within minutes. In some cases, it might take up to 24 to 48 hours if extra verification is needed. When your account is approved, you’ll gain immediate access to your online dashboard, and your Bluevine business debit card will be mailed out, arriving within a week or so.

There’s no minimum opening deposit, and you can fund your account by linking an external bank account whenever you’re ready. Everything from bill payments to mobile check deposits is ready to go as soon as you log in.

What You’ll Need to Qualify

To be eligible for a Bluevine line of credit, your business should meet a few basic requirements:

- At least 6 months in business

- A minimum FICO score of 625

- Monthly revenue of at least $10,000

Once approved, you can draw funds whenever you need them, and repayments are automated weekly or monthly, depending on your terms.

>> Open a Bluevine Account in a Few Steps >>

Bluevine Review Frequently Asked Questions

Does Bluevine Support Zelle or Other Instant Transfers?

Not currently. Bluevine doesn’t integrate with Zelle or offer instant peer-to-peer transfers. However, it does support ACH payments, wires, and bill pay features directly through the app.

Can I Use Bluevine for Personal Banking?

No. Bluevine is exclusively for business banking. If you’re looking for personal accounts, you’ll need to explore other FinTech solutions.

Can I Open a Joint Account With Bluevine?

Not at this time. Bluevine currently supports only one primary account holder per business account. However, you can add team members with limited-access user roles.

>> Open Your Bluevine Account Today! >>

Final Verdict: Is Bluevine Worth It in 2025?

Small businesses in 2025 should consider Bluevine as their top business banking solution because it offers modern mobile features designed for their needs. The high-yield business checking account at Bluevine stands out from traditional banks because it offers no monthly fees, unlimited transactions, and a competitive line of credit options.

The service doesn’t suit every business requirement. Businesses that conduct most of their transactions in cash and require face-to-face banking services will find Bluevine to be insufficient. The absence of 24/7 customer service availability creates a disadvantage for businesses needing immediate assistance.

The value Bluevine provides exceeds expectations for freelancers together with entrepreneurs, and digital-first businesses. The platform gives you essential financial tools without imposing unnecessary burdens. You earn interest, you avoid fees, and you get easy access to your money from anywhere.

So, is Bluevine worth it? Most small business owners, together with self-employed professionals, should choose Bluevine without any doubt.

>> Check Out the Best Options on Bluevine! >>

Noah is an American copywriter on a mission to help clarify the nuances of the business world through unique insights stemming from backgrounds in both engineering and the medical field. When not working, you’ll likely find him running or traveling.